The word platform is defined by Oxford English Dictionary as:

“a raised level surface on which people or things can stand, usually a discrete structure intended for a particular activity or operation”

The modern and present understanding of the concept has evolved through three different chronological, though overlapping, waves that focuses on prod-ucts, technological systems and transactions.

The first wave emerged from product developers, who used the term for product genera-tions or families for a specific firm, such as Samsung’s Galaxy phone series. This view meant that the platform functioned as a foundation for various customer segments, service and product variations. Therefore, the platform characteristics focuses on the high degree of modularisation and variation.

The second wave was brought by technological strategist who “identified platforms as valuable points of control (and rent extraction) in an industry”. This indicate that income was generated without producing any actual value, but instead at the expense of the whole economy network. One example of this was operating system Windows decision to make their own web browser a default, which distorted the browser competition remarkably.

The third wave is formulated by industrial economists, who describes the platform as a marketplace for products, services, firms, or institutions that mediate transactions among two or more parties. An example of this is Amazon, an e-commerce retailing company, who connects sellers and buyers of retail products.

Network Effects

In literature there are a lot of different interpretations regarding the term “platform”, but two perspectives remain predominant that is external and internal platforms. Gawer and Cusumano defines internal platform as a “set of assets organized in a common structure from which a company can efficiently develop and produce a stream of derivative products”, while external platform is “products, services, or technologies that act as a foundation upon which external innovators, organized as an innovative business ecosystem, can develop their own complementary products, technologies, or services”.

It is evident that the external platforms face challenges in terms of creating fruitful network effects. Network effects are defined as the additional utility that an economic agent benefit and gains when other agents are consuming the same good or service. Also network effect give cause to a “generativity” phenomenon, which is defined as “a technology’s overall capacity to produce unprompted change driven by large, varied and uncoordinated audiences” (Elaluf-Calderwood et al., 2011). In a platform context this refers to its ability to produce, create, and generate new content, without input or addi-tional help from its original creators.

Direct and Indirect Network effects

Network effects can further be categorised into direct and indirect effects, where:

“direct network effects are generated through a direct physical effect from the number of purchasers, whereas indirect network effects are market mediated effects”.

The generation of network effects is a very crucial and essential factor from a platform perspective, because without users the platform appears useless. This paradox gives rise to “chicken-and-egg” problem which all platforms need to tackle before their establishment.

Finally, a digital platform can be defined as a “IT systems and their common operating standards who different stakeholders – users, providers and other stakeholders across or-ganizational boundaries – together realise and embodies for value generating activities”. Also these platforms are characterized by its different actors whom create, provide, and maintain complementary products and services through different dis-tribution channels, but within the frame of common established platform rules and user experience requirements. In addition, a typical characteristic for these digital platform administrators is to encourage, attract, and commit various stakeholders to the platform; in order to generate network effects that produces overall economic gains for all interact-ing parties.

It can be concluded that in recent decade there has emerged loads of digital platforms that has proven to be extremely valuable. For example, half of the twenty most valuable cor-porations on the New York Stock Exchange (NYSE) considers themselves as digital plat-form companies. Henceforth, three main shifts in the aspect of competition that digital platforms are reckoned that are causing:

from resource control to resource orchestration; from internal optimization to external interaction; and focuses shifting from customer value to focus on ecosystem value.

Because of these shifts the digital platforms are showing the way for a new emerging economy, that is a platform focused digital economy.

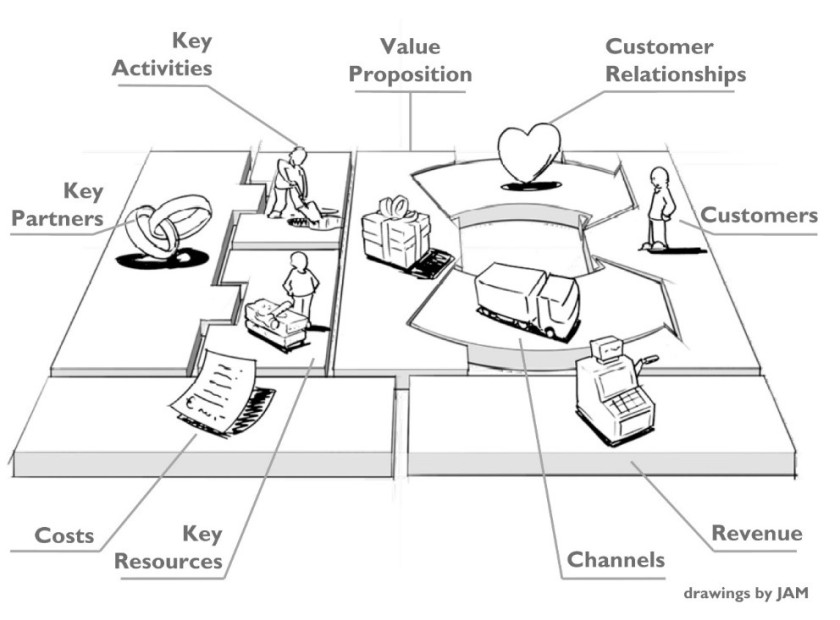

Digital Platform Structure and Classification

There are identified four basic structural types of interacting actors that can be found in every platform ecosystem. The structure is divided into owners, providers, producers, and consumers. Where the platform actors are: the owner, exhibits control over the intellectual property and governance; the providers, who “serve as the platforms interface with users”; and producers, who create offerings that the final consumers use. Thus in order to manage digital platforms, it is of great importance to understand each of the different actors and their dynamic relationships.

Evans and Gawer (2016) introduces a framework that classifies platforms into four different types, or groups. These platform types can further be ordered and visualised into a 2×2 matrix illustrated in Figure 8, whose vertical axis refer to the amount of knowledge is known about the end customer and correspondingly the horizontal axis refer to the required network effects.

Figure. Matrix illustrating the classification of platforms.

The transaction platform can be a product, service, or technology that functions as an intermediary for exchanging transactions between different users, buyers, or suppliers. The basic principle is that the transactions result in reorganiza-tion of both resources and assets by digital means and that these platforms are character-ized by its tendency to monopolise its customers. For example, Uber and PayPal are transaction platforms.

An innovation platform is a “product, service or technology that serves as foundation for which other firms can develop complementary technologies, products or services”, for example both Amazon and Google are innovation platforms. In essential this means that anyone can use the platforms resources freely and no one are eligible to own the platforms customers.

Investment platforms are owned by companies that are developing “a platform strategy and act as a holding company, active platform investor or both”. The idea is to provide with a broader solution offering to its customers, e.g., Santander and Naspers.

The integration platform “is a technology, product or service that is both a transaction and innovation platform”. A typical characteristic for integration plat-forms is that it attempts to convince and attract various parties to join the platform because of its plausible economical gains from the arising network effects. The Apple iStore concept is an example of an integration platform.

Connecting People and Economics – A Bad thing?

Are the new emerging platforms a trampoline for growth and opprotunites, or more like a malevolent spider-webb with negative and polarlizing side-effects for the society as a whole? Platfoms, such as Apple; Amazon; and Ebay, surely makes our lives more practical/easier and improves the classical functionality of a market for exchanging goods. However, I am not so sure about the new platforms that concerns with intangibles, such as Facebook and Google. Do these improve our everyday life? The answer is clear as mud. On short term these do provide with improvements, but what about long term effects? Are an overflow of “bad” information and cyber-relationships good for us?

Time will tell, but one thing is sure that these issues needs more attention and discussion. Regardless, my strong personal view is that some intangible cyber platform “relationships” are align with the follwing qoute:

“F**in’ see why they call this bullshit a “relationship” – ships sink”

/Drill

Information is increasingly being perceived as a valuable asset in today’s modern society, de facto that in some occurrences information is by far the most valuable asset of a business and its activities. This tendency is refered often with the quote: “data is the new oil”.

Information is increasingly being perceived as a valuable asset in today’s modern society, de facto that in some occurrences information is by far the most valuable asset of a business and its activities. This tendency is refered often with the quote: “data is the new oil”.